Next: Optimal Insurance

Up: sharesl

Previous: Investment in CD and

The optimal portfolio depends on the utility function  .

Consider, for example, the optimal portfolio for three different

utility functions.

.

Consider, for example, the optimal portfolio for three different

utility functions.

The first utility function is linear

|

|

|

(11) |

This function is for "rich" persons. Rich persons want to maximize the average wealth. They are not emotional about

accidental losses or gains. In the linear case

(11), the optimal portfolio is to invest all the

capital in an object with the highest product  .

.

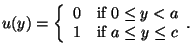

The

second utility function is for "prudent" persons which averse

risk

|

|

|

(12) |

Here  is a risk threshold.

is a risk threshold.

denotes the

maximal return of invested capital (see expression

(4)). If

denotes the

maximal return of invested capital (see expression

(4)). If

then, in the

risk-averse case the optimal decision is

then, in the

risk-averse case the optimal decision is

. Here one divides the capital equally

between all the objects1.

. Here one divides the capital equally

between all the objects1.

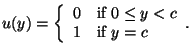

The third utility function is for "risky" persons. Risky persons are

ready to risk for the great win  .

.

|

|

|

(13) |

Here one invests all the capital in the object with highest

wealth return. Therefore,  , if

, if

.

.

These examples

are abstract. An average person behaves "risky," if

only a small part of his resources is involved. The same person

behaves prudently, if all his wealth is at stake. There is

a point  between areas of risky and prudent behavior. At this point an average person

behaves like the "rich" one. Here is an example

between areas of risky and prudent behavior. At this point an average person

behaves like the "rich" one. Here is an example

Here is a boundary point between risky and prudent areas.

Next: Optimal Insurance

Up: sharesl

Previous: Investment in CD and

2002-11-04