Next: Optimal Portfolio, Special Cases

Up: Expected Utility

Previous: Investment in CD

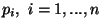

Investing in CD, the interests  are defined by contracts.

Only the reliabilities

are defined by contracts.

Only the reliabilities

of banks are uncertain.

Investing in stocks, in addition to reliabilities

of banks are uncertain.

Investing in stocks, in addition to reliabilities

of companies, their future stock rates are uncertain, too. The predicted stock rates are defined by a coefficient

of companies, their future stock rates are uncertain, too. The predicted stock rates are defined by a coefficient  that shows the relation between the present and the predicted stock rates. The prediction "horizon" is supposed to be the same as the maturity time of CD.

that shows the relation between the present and the predicted stock rates. The prediction "horizon" is supposed to be the same as the maturity time of CD.

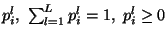

To simplify the model suppose that one predicts  different values of relative stock rates

different values of relative stock rates

with corresponding estimated probabilities

with corresponding estimated probabilities

.

.

In this case,

one may define probabilities  of discrete values of

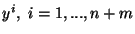

wealth

of discrete values of

wealth

by exact expressions.

The expressions for CD remains the same. Therefore,

we shall consider only stocks assuming that

by exact expressions.

The expressions for CD remains the same. Therefore,

we shall consider only stocks assuming that  and

and  .

Then

.

Then

Here

.

The reliabilities

.

The reliabilities  , the stock rate predictions

, the stock rate predictions  and their estimated probabilities

and their estimated probabilities  are defined by

experts, possibly, with the help of time series models such as ARMA

For example, maximal values of multi-step prediction

are considered as "optimistic" estimates. The minimal values- as "pessimistic" ones. The average values of multi-step prediction are regarded as "realistic" estimates.

are defined by

experts, possibly, with the help of time series models such as ARMA

For example, maximal values of multi-step prediction

are considered as "optimistic" estimates. The minimal values- as "pessimistic" ones. The average values of multi-step prediction are regarded as "realistic" estimates.

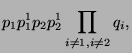

Here is a simplest illustration were  and . In this case from (5) (10)

the probabilities

and . In this case from (5) (10)

the probabilities  of wealth returns

of wealth returns

are

are

Here

.

.

Next: Optimal Portfolio, Special Cases

Up: Expected Utility

Previous: Investment in CD

2002-11-04