Next: Nash Equilibrium

Up: sharesl

Previous: Optimal Portfolio, Special Cases

In this section the optimal insurance is regarded as a special case

of optimal investment.

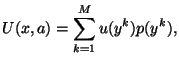

Then the expected utility at the end of the next year

|

|

|

(15) |

where  is a probability to get a wealth

is a probability to get a wealth  ,

,

is an utility function of this wealth .

is an utility function of this wealth .

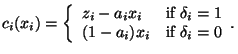

Here

is a vector which components

is a vector which components

define rates of insurance charges

for different objects

define rates of insurance charges

for different objects  .

Suppose that

.

Suppose that

and

|

|

|

(16) |

The product  denotes insurance charge of the object

denotes insurance charge of the object  ,

,

is insurance policy of the object ,

is insurance policy of the object ,

is market value of the object ,

is market value of the object ,

, if the object survives,

, if the object survives,

, otherwise,

, otherwise,

is a survival probability of the object .

is a survival probability of the object .

For example:

,

,

,

,

where

.

.

2002-11-04