Next: Optimization of AR parameters

Up: Exchange Rate Forecasting, Time

Previous: Definition of Residuals

Minimization of Residuals of ARMA Models

We consider an algorithm for optimization of parameters of the ARMA model.

This model is simple and may be regarded as a good first approximation.

Denote by  the value of

the value of  at the moment

at the moment  . Denote by

. Denote by

a vector

of auto-regression (AR) parameters, and by

a vector

of auto-regression (AR) parameters, and by

a vector of moving-average (MA) parameters.

a vector of moving-average (MA) parameters.

|

|

|

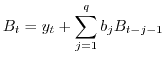

(5) |

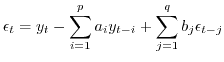

The residual

|

|

|

(6) |

or

|

|

|

(7) |

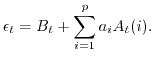

Here

|

|

|

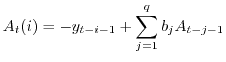

(8) |

and

|

|

|

(9) |

where  and

and  .

.

Subsections

Next: Optimization of AR parameters

Up: Exchange Rate Forecasting, Time

Previous: Definition of Residuals

mockus

2008-06-21