Next: Evaluation of ARMA Prediction

Up: Minimization of Residuals of

Previous: Optimization of MA parameters

Predicting "Next-Day" Rate

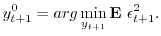

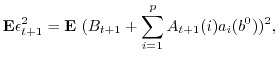

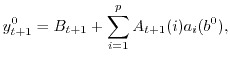

We minimize the expected "next-day" squared deviation

using the data available at the moment

using the data available at the moment

|

|

|

(18) |

Here

|

|

|

(19) |

where the optimal parameter  was obtained using the data available at the day

.

Variance (1.20) is minimal, if

was obtained using the data available at the day

.

Variance (1.20) is minimal, if

|

|

|

(20) |

because the expectation of  is

is

under the assumptions.

under the assumptions.

mockus

2008-06-21