Next: Single Company Insuring Multiple

Up: Single Company Insuring Single

Previous: Single Company Insuring Single

First we fix the initial values, the "Contract-Vector"

. The transformed values, the

"Fraud-Vector"

. The transformed values, the

"Fraud-Vector"  , are obtained by

maximizing the utilities

, are obtained by

maximizing the utilities  and

and  respectively. The maximization is

performed under the assumption that a partner

honors the contract

respectively. The maximization is

performed under the assumption that a partner

honors the contract

|

|

|

(21) |

|

|

|

(22) |

Formally, condition (22) transforms the vector

into the vector

into the vector  . To make expressions

shorter denote this transformation by

. To make expressions

shorter denote this transformation by

|

|

|

(23) |

One may obtain the equilibrium at the fixed point  , where

, where

|

|

|

(24) |

The fixed point exists, if the feasible set  is convex

and all the profit functions are convex

[2]. We obtain the equilibrium directly by

iterations (23), if the transformation is contracting

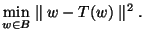

[4]. If not, then we minimize the square deviation

is convex

and all the profit functions are convex

[2]. We obtain the equilibrium directly by

iterations (23), if the transformation is contracting

[4]. If not, then we minimize the square deviation

|

|

|

(25) |

The equilibrium is achieved, if the minimum (25)

is zero. If the minimum (25) is positive then the equilibrium does not exist. That is a theoretical conclusion.

In statistical modeling, some deviations are inevitable. Therefore,

we assume that the equilibrium exists, if the minimum is

not greater then modeling errors.

Next: Single Company Insuring Multiple

Up: Single Company Insuring Single

Previous: Single Company Insuring Single

2002-11-04