Next: Search for Equilibrium

Up: Nash Equilibrium

Previous: Nash Equilibrium

In this section the optimal insurance is regarded as a

problem of insurance company.

We start from the simplest case of single company

insuring a single object.

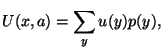

The expected utility of this object

|

|

|

(17) |

where  is a probability of wealth

is a probability of wealth  ,

,

is an utility function of the wealth .

is an utility function of the wealth .

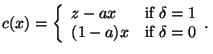

Here  is the rate of insurance charge.

is the rate of insurance charge.

Suppose that

and

|

|

|

(18) |

Here  is the market value of the object,

is the market value of the object,

the product  denotes insurance charge of the object.

denotes insurance charge of the object.

is insurance policy of the object.

is insurance policy of the object.

, if the object survives,

, if the object survives,

, if not.

, if not.

is a survival probability of the object.

is a survival probability of the object.

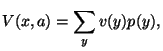

The expected utility of the insurance company

|

|

|

(19) |

where

is a probability of profit ,

is an utility function of the profit .

is an utility function of the profit .

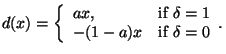

Suppose that

and

|

|

|

(20) |

Here insurance policy  is defined by the owner of object which

maximizes his utility

(15) depending on the rate of insurance charge .

The equilibrium between interests of the company and the customer

is achieved when both insurance policy and

insurance charge satisfies Nash conditions.

is defined by the owner of object which

maximizes his utility

(15) depending on the rate of insurance charge .

The equilibrium between interests of the company and the customer

is achieved when both insurance policy and

insurance charge satisfies Nash conditions.

Subsections

Next: Search for Equilibrium

Up: Nash Equilibrium

Previous: Nash Equilibrium

2002-11-04