Next: Multi-Step Prediction

Up: Auto-Regression Fractionally-Integrated Moving-Average Models

Previous: Minimization of Residuals

Table 1.2 shows some results obtained using the ARFIMA model [14]. Parameters  and

and  were estimated using daily exchange rates of $/£,

and DM/$, and closing rates of

AT&T and Intel Co stocks.

were estimated using daily exchange rates of $/£,

and DM/$, and closing rates of

AT&T and Intel Co stocks.

Table 1.2:

Estimated parameters and of ARFIMA models.

|

|

|

|

|

$/ |

-1.195 |

-0.169 |

0.0005 |

1.51675 |

| DM/$ |

-1.019 |

0.0120 |

0.0007 |

1.60065 |

| AT&T |

-1.017 |

0.0118 |

0.00005 |

9.83208 |

| Intel Co |

0.9975 |

0.0055 |

0.012 |

7.35681 |

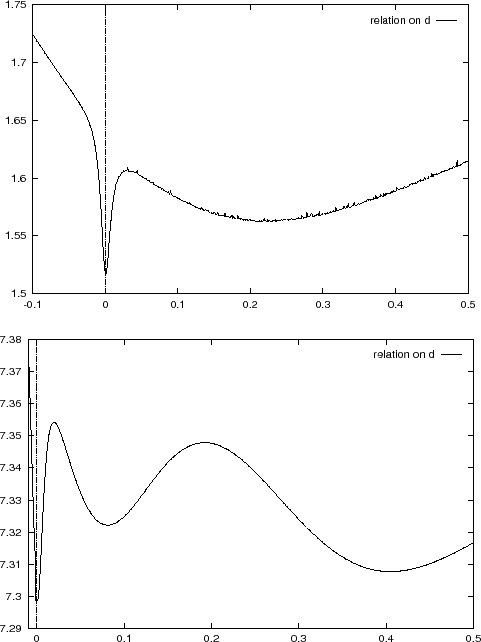

It is clear from Table 1.2 that 's for all the time series

are

very close to zero (see also Figures 1.3 and 1.4).

Figure 1.3:

Log-sum (1.45) as a function of the parameter

![$d \in [-0.1,0.5]$](img3.png) regarding the $/ exchange rate

regarding the $/ exchange rate

Figure 1.4:

Log-sum (1.45) as a function of the parameter

![$d \in [-0.01,0.5]$](img5.png) regarding the Intel Co stocks closing rate

regarding the Intel Co stocks closing rate

|

Hence, following the traditional approaches to testing for long memory processes (see, for example,[1,20,2]) we may conclude that the underlying

stochastic processes generating exchange rates of $/£and DM/$ , and closing rates of AT&T and Intel Co stocks,

do not exhibit persistence and are stationary.

That contradicts the visual impression of the corresponding data

(see Figures 1.5 and 1.11).

This apparent contradiction may be resolved by dropping the assumption that the parameters  of the ARFIMA model remain constant. This assumption is common for most of the traditional methods. An alternative is structural stabilization models described in chapter 1.10.

of the ARFIMA model remain constant. This assumption is common for most of the traditional methods. An alternative is structural stabilization models described in chapter 1.10.

Next: Multi-Step Prediction

Up: Auto-Regression Fractionally-Integrated Moving-Average Models

Previous: Minimization of Residuals

mockus

2008-06-21