Predictions often depend on several factors

In such a case multi-dimensional ARMA should be used.

Denote by

![]() the main statistical component and by

the main statistical component and by

the external factors. In such a case we extend the traditional ARMA model this way

the external factors. In such a case we extend the traditional ARMA model this way

we minimize the squared deviation

we minimize the squared deviation

At fixed ![]() the optimal values of

the optimal values of ![]() are defined by a system of linear equations

calculated from the condition that all the partial derivatives

are defined by a system of linear equations

calculated from the condition that all the partial derivatives

![]() of the sum (1.60) are zero.

Thus obtaining the least squares estimates

of the sum (1.60) are zero.

Thus obtaining the least squares estimates

![]() at given

at given

![]() we have to solve

we have to solve ![]() linear equations with

linear equations with ![]() variables

variables

![]() (see chapter 1.3 for details).

(see chapter 1.3 for details).

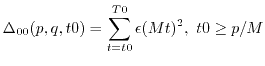

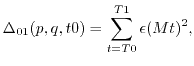

The optimization of the discrete structural variables is performed using a different data set that starts at ![]() and ends at

and ends at ![]() while keeping the previous optimal values of the state variables

while keeping the previous optimal values of the state variables ![]() and

and ![]() obtained by minimization of the sum

obtained by minimization of the sum

using the data from

using the data from ![]() to

to ![]() .

Here the sum

.

Here the sum