The traditional time series models assume that their parameters do not change. Examples are parameters ![]() of the ARMA model, parameters

of the ARMA model, parameters ![]() of the ARFIMA model, parameters

of the ARFIMA model, parameters ![]() of the BL model, and parameters

of the BL model, and parameters

![]() of the ANN model.

of the ANN model.

The variability of parameters of models describing the financial data such as stock rates and the currency exchange rates can be partially explained by the changes of economical conditions. However this variability is there even in the stable economical conditions. The reason is the "Feed-Back" processes. It is well known that the predictions may influence the supply and demand and consequently the future data.. In such cases the statistical best fit models should be complemented or replaced by the game-theoretical equilibrium models. However there is the possibility that the equilibrium model would be namely the Wiener process. That means that the market rates in economics are governed by the similar model as the Brownian motion in physics and are as unpredictable as the movement of individual molecules in gases. Table 1.1 shows that the simplest Wiener process, called as the Random Walk (RW), predicts the financial data at least as well as Arma models.

The objective of traditional time series models is to define such parameters that minimize a deviation from the available data.

One may call them as the best fit models.

The goodness of fit is described by continuous parameters ![]() called as state variables. For example, in the ARMA model (see expression (1.1)) the state variables

called as state variables. For example, in the ARMA model (see expression (1.1)) the state variables

![]() .

.

If the parameters remain constant in the future, then models that fit best to the past data will predict the future data as well. Otherwise, the best fit to the past data can be irrelevant or even harmful for predictions.

Models are needed which are not sensitive to the changes of system parameters. Such models may predict the uncertain future better by eliminating the nuisance parts from the structure of the model.

Trying to solve this problem we introduce a notion of the model structure. The model structure is determined by the Boolean parameters

![]() called as structural variables. A structural variable is equal to unit if the corresponding component of time series model is included . Otherwise, the structural variable is equal to zero. For example, in the ARMA model

called as structural variables. A structural variable is equal to unit if the corresponding component of time series model is included . Otherwise, the structural variable is equal to zero. For example, in the ARMA model

![]() . Here

. Here

![]() , if the parameter

, if the parameter ![]() is included into the ARMA model and

is included into the ARMA model and ![]() , otherwise

, otherwise![]() .

We search for such structure

.

We search for such structure ![]() of the model that minimizes the prediction errors in the changing environment.

of the model that minimizes the prediction errors in the changing environment.

To achieve this we divide available data

![]() into two parts

into two parts

![]() and

and

![]() .

.

The first part ![]() is for estimation of continuous parameters

is for estimation of continuous parameters ![]() which depends on Boolean structural parameters

which depends on Boolean structural parameters ![]() . The estimation is performed for a set of all feasible

. The estimation is performed for a set of all feasible ![]() by minimizing the least square deviation.

by minimizing the least square deviation.

The second part ![]() is used to select such

is used to select such ![]() that

minimize the least square deviation. This means that the second part

that

minimize the least square deviation. This means that the second part ![]() is for estimation of Boolean structural parameters.

is for estimation of Boolean structural parameters.

Denote by ![]() the predicted value of a model

the predicted value of a model ![]() with fixed parameters

with fixed parameters ![]() using the data

using the data

![]() . The difference between the prediction and the actual data

. The difference between the prediction and the actual data ![]() is denoted by

is denoted by

![]() . Denote by

. Denote by ![]() the fitting parameters

the fitting parameters ![]() which minimize the sum of squared deviations

which minimize the sum of squared deviations

![]() using the first data set

using the first data set ![]() at fixed structure parameters

at fixed structure parameters ![]() .

.

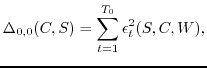

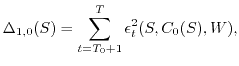

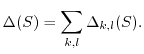

We consider two data sets ![]() and

and ![]() just for simplicity.

One may partition the data

just for simplicity.

One may partition the data ![]() into many data subsets

into many data subsets

![]() . In this case we minimize the sum

. In this case we minimize the sum

|

(53) |

|

(54) |

The usefulness of the structural stabilization follows from the observation that any optimal

estimate of time series parameters using a part ![]() of the data

of the data

![]() is optimal for another part

is optimal for another part ![]() only if all the parameters remain the same. Otherwise one may obtain a better estimate eliminating the changing parameters from the model. For example in the case of changing parameters

only if all the parameters remain the same. Otherwise one may obtain a better estimate eliminating the changing parameters from the model. For example in the case of changing parameters

![]() of the ARMA model the best prediction may be obtained by elimination of all the parameters except

of the ARMA model the best prediction may be obtained by elimination of all the parameters except ![]() (see Table 1.1).

(see Table 1.1).