Next: Minimization of Residuals

Up: Auto-Regression Fractionally-Integrated Moving-Average Models

Previous: Auto-Regression Fractionally-Integrated Moving-Average Models

The stationarity of time series is assumed in ARMA, ANN, and BL models. That is a simplification of reality.

A well known source of non-stationarity is a linear component, the trend.

One can eliminate the trend by differencing, since derivatives of linear functions are constant. The elegant extension of this idea is the

Auto-Regression Fractionally-Integrated Moving-Average Model (ARFIMA).

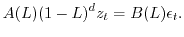

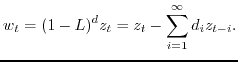

We define an ARFIMA![[*]](file:/usr/share/latex2html/icons/footnote.png) process as the folowing time series

process as the folowing time series

|

|

|

(35) |

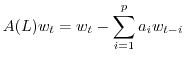

Here

|

|

|

(36) |

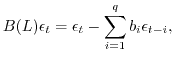

and

|

|

|

(37) |

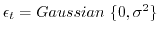

where

.

.

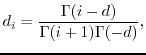

We define the transformation  as follows:

as follows:

|

|

|

(38) |

Here

|

|

|

(39) |

where  is a fractional integration parameter, and

is a fractional integration parameter, and  is a

gamma function.

is a

gamma function.

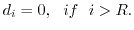

We assume that

|

|

|

(40) |

We truncate sequence (1.39)

|

|

|

(41) |

Here  is the truncation parameter, the number of non-zero components.

is the truncation parameter, the number of non-zero components.

Next: Minimization of Residuals

Up: Auto-Regression Fractionally-Integrated Moving-Average Models

Previous: Auto-Regression Fractionally-Integrated Moving-Average Models

mockus

2008-06-21